Can You Reopen a Hurricane Insurance Claim After Settlement in Florida?

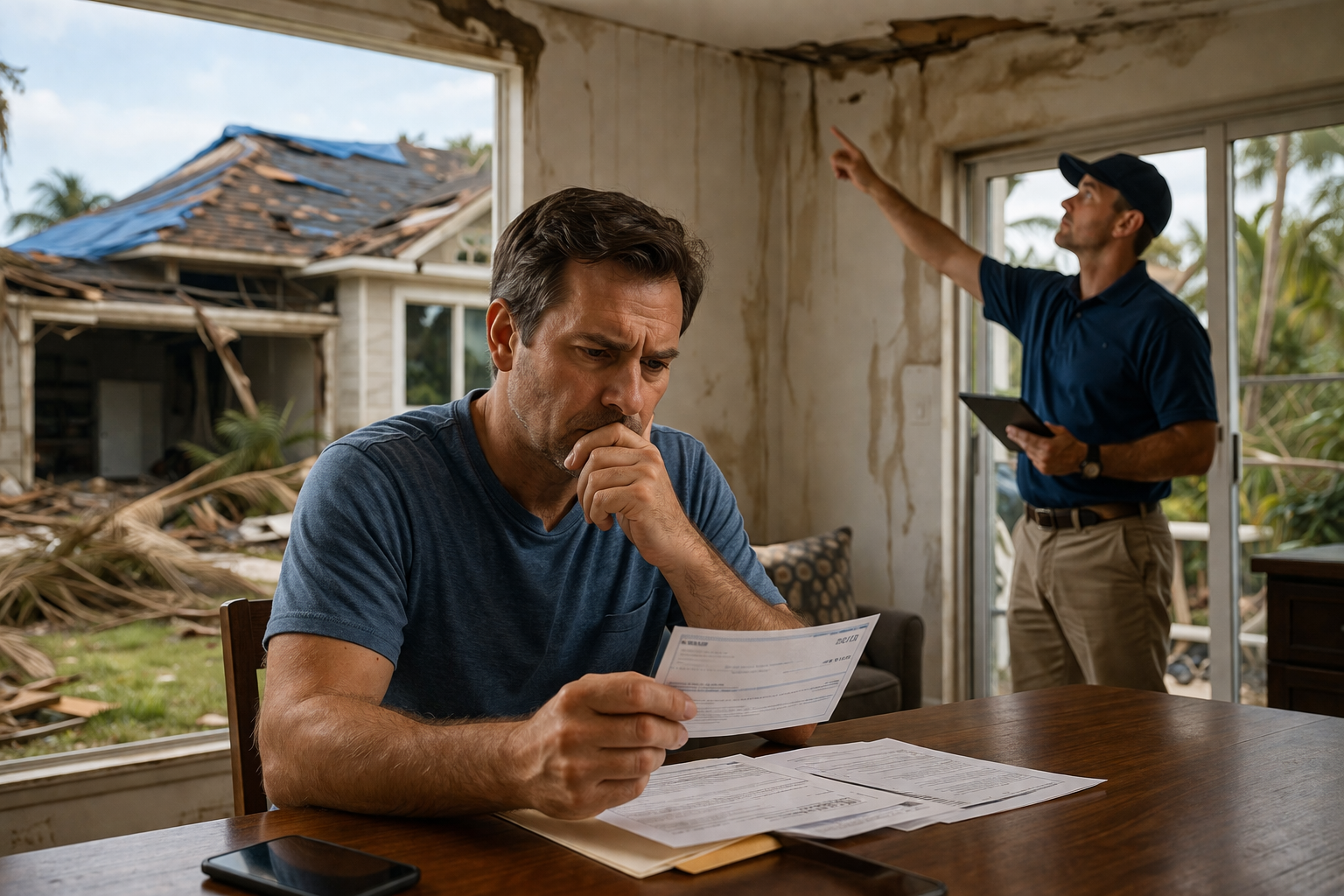

After a hurricane, most homeowners just want to move on and rebuild their lives quickly. Many accept the first settlement offer their insurance company presents without question. But weeks or months later, hidden damage often surfaces that was not caught during the initial inspection.

The payout that seemed fair suddenly does not cover the full cost of repairs. This raises an important question: can you reopen a hurricane claim after you have already settled? The answer depends on Florida law, your policy language, and what documents you signed. CMS Law Group helps homeowners understand their options and fight for the compensation they truly deserve.

Is It Too Late to Reopen Your Hurricane Insurance Claim?

In some cases, you can reopen a hurricane claim even after receiving a settlement payment. However, whether you can depends on several important factors specific to your situation. Your insurance policy terms play a major role in what options remain available to you. Whether you signed a full release of liability is one of the most critical legal distinctions.

New or undiscovered damage found after settlement can sometimes support a supplemental or reopened claim. Evidence that your insurer acted in bad faith may also open additional legal paths for recovery. Each case is different, and speaking with an attorney is the best way to know where you stand.

Common Reasons Homeowners Try to Reopen a Hurricane Claim

Many homeowners only realize their settlement was insufficient long after the check has cleared. Hidden damage often goes unnoticed during rushed post-storm inspections. Here are the most common reasons homeowners seek to reopen a hurricane claim:

- Hidden structural damage appears later — Damage to trusses, framing, or foundations is not always visible right after a storm

- Initial payout was too low — The settlement amount fails to cover the actual cost of full restoration and repairs

- Additional repair costs exceed the estimate — Contractors often uncover deeper damage once demolition or repair work begins

- Insurance adjuster overlooked key damage — Adjusters working quickly after major storms sometimes miss damage to roofing, siding, or interiors

- Contractor findings reveal new issues — Licensed contractors may identify problems the insurer’s adjuster failed to document or include

When Reopening a Claim May Be Possible Under Florida Law

Florida law provides certain protections for homeowners who discover that their settlement did not fully cover their hurricane losses. Several specific circumstances may allow you to pursue additional compensation after a settlement has been reached. Here is a closer look at when reopening may be a valid legal option:

New or Supplemental Damage Is Discovered

If damage was not visible during the original inspection, you may have grounds to file a supplemental claim. Mold growth, roof leaks, and structural weakening often develop or become visible weeks after the initial storm. This type of newly discovered damage is one of the strongest bases for reopening a hurricane claim in Florida.

The Insurance Company Underpaid the Claim

Lowball settlement offers are unfortunately common after major hurricane events in Florida. If your insurer’s estimate missed key line items or severely undervalued the damage, you may be able to challenge it. An attorney can compare the payout to actual repair costs and identify where underpayment occurred.

No Full Release of Liability Was Signed

Not all settlements include a full and final release of liability from the homeowner. If you accepted payment without signing a complete release, supplemental claims may still be possible. This legal distinction is critical and often overlooked by homeowners who settle without reviewing documents carefully.

Evidence of Insurance Bad Faith

Florida law holds insurers accountable for bad faith practices during the claims process. If your insurer delayed your claim, misrepresented your coverage, or used unfair denial tactics, you may have a bad faith claim. Bad faith cases can result in additional compensation beyond the original policy limits.

When You May NOT Be Able to Reopen Your Claim

Reopening a hurricane claim is not always possible, and it is important to understand the limitations honestly. Certain circumstances close the door on additional recovery, no matter how strong your case feels. Here is when reopening a claim may no longer be a legal option:

You Signed a Full and Final Settlement Release

If you signed a document releasing your insurer from all future liability, reopening your claim becomes extremely difficult. A full and final release is a binding legal agreement that typically ends your right to additional compensation. Before signing any settlement documents, always have an attorney review the language carefully first.

The Legal Deadline Has Passed

Florida law sets strict deadlines for filing or reopening hurricane insurance claims after a storm. Missing these deadlines can permanently eliminate your right to pursue any additional recovery from your insurer. Time is one of the most important factors in any hurricane claim situation.

No New Evidence or Damage Exists

If there is no new evidence and the damage has not changed since your original settlement, reopening is unlikely. Insurers and courts require a factual basis for revisiting a closed claim after payment has been issued. Without new findings or proof of underpayment, options for additional recovery become very limited.

Florida Deadlines for Hurricane Insurance Claims

Florida has strict deadlines that directly affect your ability to reopen a hurricane claim after settlement. Depending on your policy and the type of claim, the statute of limitations is generally one to two years from the date of loss. Some policies include even shorter notice periods that homeowners often miss entirely.

Acting quickly after discovering new damage or underpayment is absolutely critical. Every day you wait brings you closer to a deadline that could eliminate your legal options completely. Do not assume you have time. Contact an attorney as soon as you believe your claim may not have been fully resolved.

Steps to Take If You Want to Reopen Your Hurricane Claim

Taking the right steps early gives you the best chance of successfully reopening your hurricane claim. Acting carefully and deliberately protects your rights and strengthens your legal position significantly. Here is what you should do right away:

Review Your Insurance Policy and Settlement Documents

Pull out your original policy and any settlement paperwork you signed after the storm. Look for language about supplemental claims, releases of liability, and deadlines for additional filings. Understanding exactly what you agreed to is the foundation of any strategy to reopen your claim.

Document All New or Missed Damage

Photograph and video all newly discovered or previously overlooked damage in detail right away. Write detailed notes describing where the damage is, when it appeared, and how severe it seems. Strong visual documentation creates a factual record that supports your case for reopening the claim.

Get a Second Inspection or Contractor Estimate

Hire a licensed contractor or independent adjuster to assess the full scope of your property damage. A second professional opinion can reveal damage that was missed or undervalued during the original insurance inspection. A detailed written estimate from a contractor is powerful evidence in any supplemental claim situation.

Avoid Speaking to Insurers Without Legal Guidance

Do not contact your insurance company to discuss reopening your claim without first speaking to an attorney. Anything you say can be used to limit or deny any additional recovery you may be entitled to. An attorney can communicate with your insurer on your behalf and protect your interests throughout the process.

Consult a Hurricane Insurance Attorney

A hurricane insurance attorney can review your settlement, documents, and new evidence quickly. They will tell you honestly whether you have grounds to reopen your claim and what your options are. Early legal guidance is the single most effective step you can take to protect your right to full compensation.

How CMS Law Group Helps With Reopened Hurricane Claims

CMS Law Group has helped Florida homeowners challenge underpaid and improperly closed hurricane insurance claims. Our attorneys carefully review every settlement agreement and insurance policy to identify where insurers fell short. We look for signs of bad faith, lowball tactics, and missed damage that was never properly accounted for. Once we identify the issues, we build strong documentation and evidence to support your supplemental or reopened claim. Our team handles all negotiations with your insurer and pursues litigation when necessary to protect your rights. Our goal is always to maximize your recovery and ensure you receive the full compensation your policy provides.

Your Claim May Not Be as Final as You Think. Let’s Talk.

Settling a hurricane claim does not always mean the case is permanently closed. If new damage has appeared or your payout did not cover your actual losses, you may still have options. The key is acting quickly before Florida’s legal deadlines eliminate your right to pursue additional recovery.

CMS Law Group is here to review your situation and give you honest, clear guidance. Reach out today for a free consultation and find out what your next steps should be.

CMS Law Group

12955 Biscayne Blvd. Suite 201

North Miami, FL 33181

(866) 345-2033

info@cmslawgroup.com